Malta Real Estate 2025: Prices and Risks

Malta Real Estate 2025: An Investor View on Prices, Demand, Yields, and Risks

Malta often appears on international investor radars as a stable, EU-based market with lifestyle appeal. But the 2025 data shows something important: the market is rising overall, yet performance differs sharply by property type, rental yields are modest, and foreign ownership rules can completely change what is possible.

Below is a structured, numbers-first overview of Malta property in 2025, with the key investor takeaways.

1) Price dynamics: the market rises, but not every asset rises

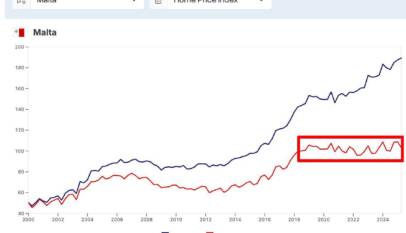

National price index (Q3 2025):

- +6.88% year over year (real, inflation-adjusted: +4.39%)

- Quarter over quarter: +0.7% (fourth consecutive quarter of growth)

However, the same period shows very different results by property type (year over year to Q3 2025):

- Apartments: +4.9% (real: +2.46%)

- Maisonettes: +3.06% (real: +0.66%)

- Terraced houses: −2.16% (real: −4.44%)

- Other houses (villas, townhouses, “house of character”): −7.23% (real: −9.39%)

Investor takeaway: Malta is not a market where “any house will do.” The headline index can be rising while certain segments are falling in real terms.

Long-cycle context also matters. The market grew strongly in real terms from 2012 to 2019, but since 2019 it has moved into a more moderate phase.

2) Demand: transactions are growing

Liquidity is not just theoretical. Deal volumes and turnover are rising:

- 2024: 12,598 transactions (+3.7%), turnover €3.53B (+8.4%)

- First 9 months of 2025: 9,788 transactions (+4.6%), turnover €2.89B (+13.4%)

Investor takeaway: the market is active, and growth is visible in real transaction flow, not just price indices.

3) Supply: construction accelerates again

New supply is increasing:

- New housing permits in 2024: 8,716 units (+7.4%)

- Q3 2025 saw a sharp surge: 3,668 units (+110.3% vs Q3 2024)

Investor takeaway: this is a double signal:

- Short term: the economy and demand look strong enough to justify more building

- Medium term: competition for tenants may increase, especially in mass-market segments

4) Rental and yields: moderate by global standards

Average gross rental yield across Malta is estimated at around 4.05% (Q2 2025).

Gross yields by location for apartments (ranges and averages as noted):

- Mainland Malta: ~3.63% to 4.29% (average ~4.03%)

- Gozo: ~3.86% to 4.25%

- St Julian’s: ~3.65% to 4.44% (one of the stronger zones)

- Sliema: ~1.75% to 3.03% (average ~2.24%)

- Valletta: ~1.15% to 2.46% (average ~1.72%)

Investor takeaway: Malta is more often a “capital preservation plus moderate rent” story than a high-yield market.

5) Who rents in Malta and why demand holds

Rental demand is supported not only by tourism but by long-term tenants driven by the labor market.

Foreign workers were estimated at 115,721 in 2023 (+19% year over year), with current estimates around 125,000 to 130,000.

Tenant composition is described roughly as:

- About 10% local

- About 17% EU

- About 74% third-country nationals (TCN)

Investor takeaway: the rental market is not empty. But low yields mean you need disciplined price selection and cost control.

6) The hardest part for investors: foreign ownership and rental rules

Malta is a “rules-first” market. Many investors underestimate how strongly legal structure affects what you can buy and how you can rent it.

For foreign buyers (including EU citizens without 5 years of residence), purchase is commonly limited to one property, often intended for personal use.

A key exception is Special Designated Areas (SDA), where purchase can be easier and less restricted.

For renting out, foreign owners often need the property to be:

- Located in an SDA, or

- A villa, or

- Covered by a Ministry for Tourism license (categories such as “superior/comfort”)

Examples of SDAs mentioned include Portomaso (St Julian’s), Tigné Point / Manoel Island, SmartCity, Fort Cambridge, Pender Place / Mercury House, Metropolis Plaza (Gzira), Fort Chambray (Gozo), and others.

Investor takeaway: you cannot select a unit in Malta the same way you might in more flexible markets. Start by confirming whether the legal regime allows your strategy.

7) A risk many people ignore: high vacancy

One unusual risk highlighted in Malta is the estimated share of empty housing stock. It is sometimes estimated around 18%, which is among the highest shares in the EU.

Investor takeaway: vacancy at a national level does not automatically mean your specific segment will struggle, but it is a sign to be careful with “copy-paste” assumptions about demand.

8) Taxes: the friction that changes the strategy

Tax treatment is a key part of the Malta story:

- Rental income tax: an ориентир around ~15% (depending on status and ownership structure)

- Tax on sale: around 12% of the transaction price (not of capital gain), which can be very unfriendly for short-term flips

There is also a note that if the seller is not a professional property trader, a final withholding tax at a rate of 5% may apply when selling within 5 years of purchase.

Bottom line: who Malta fits, and who it does not

Based on the 2025 profile, Malta tends to fit investors who want long-term holding, legal stability, and moderate rental income. It is generally not built for fast capital-gain projects or high passive income, especially once restrictions and sale tax friction are factored in.

If you still consider Malta, the smartest sequence is: legal regime first (SDA and rental permission), then location and tenant demand, then taxes and net yield, and only then the specific property.

How to Get a Language-Friendly Driving Test in Spain

If Spanish test language is your biggest barrier to getting a driving license, DGT has an …

{kind=link}